This publication explores production and marketing costs for an enterprise and strategies for choosing among enterprises. An enterprise here means an individual crop or livestock type produced to be sold through one or more market distribution channels (for example, farmers market, farm stand, restaurants). Considering these costs and strategies will help you make better decisions that could help make your farm more profitable. Specifically, this information will allow you to:

1. Determine input requirements for production and marketing, such as chemicals, fertilizer, fuel, labor, and packaging materials

2. Prepare a cash-flow system necessary to support loan applications

3. Determine the amount you can afford to pay for land rent, marketing space, and other capital assets used in your production and marketing

4. Develop a sound marketing plan, which begins with choosing the appropriate product mix

General Budget Analysis: Getting a handle on costs

In order to achieve a profitable enterprise in the long run, it is essential to understand your production and marketing costs. Your profit equals your gross returns minus your production and marketing costs. Gross returns are calculated by multiplying prices received for each product by the quantity of that product produced and sold. Production and marketing costs include both variable and fixed costs. Variable costs change with business volume; that is, with the number of acres planted, plants raised, or products sold. They include inputs such as fertilizer, fuel, repairs, hired labor, and packaging. Fixed costs do not vary with production volume and are charged to the business even if there’s no production. Fixed costs include depreciation, interest, hazard insurance, property taxes, housing, and capital expenditures.

As a farm business becomes more complex, for example by adding organic certification, post-harvest handling facilities, or processing equipment, there are new costs to factor into your calculations. The same rules apply for allocating them to the variable or fixed cost categories.

Major fixed costs

Depreciation and interest, which are costs of owning an asset, are prorated over the useful life of the asset. Annual straight-line depreciation is calculated by subtracting the salvage value of an asset from its initial investment value, and then dividing the remainder by the years of useful life. For example, spending $5,000 for an asset with a 10-year life and a $500 salvage value would result in an annual depreciation of $450:

($5,000 – $500) ÷ 10 years = $450

If the piece of machinery was used for production on 10 acres, the per-acre depreciation to include in production costs would be $45:

$450 ÷ 10 acres = $45/acre

The straight-line depreciation method is suitable for developing conventional cost estimates, but other depreciation methods may be more appropriate for calculating income tax liability. This is a good topic to discuss with your tax adviser.

Interest cost, the second major component of annual, fixed ownership costs, is calculated by determining the average investment and multiplying by the applicable rate of interest. The average investment is simply the initial investment plus an estimated salvage value, divided by 2. The annual interest for a $5,000 investment with a $500 salvage value and a long-term interest rate of 4 percent would be $110:

($5,000 + $500) ÷ 2 = $2,750; $2,750 x 0.04 = $110

Using the 10-acre example, the interest component of the annual ownership cost would be $11.00/acre:

$110 ÷ 10 acres = $11/acre

Include interest as an ownership charge whether or not you borrowed to finance the machinery or equipment, because there is an “opportunity cost” of having money tied up in machinery. In other words, the money could be earning interest elsewhere if it were not invested in those assets. If the asset is debt financed, include the actual interest charge as a cash expense.

Fixed and Variable Costs for Tribble Production

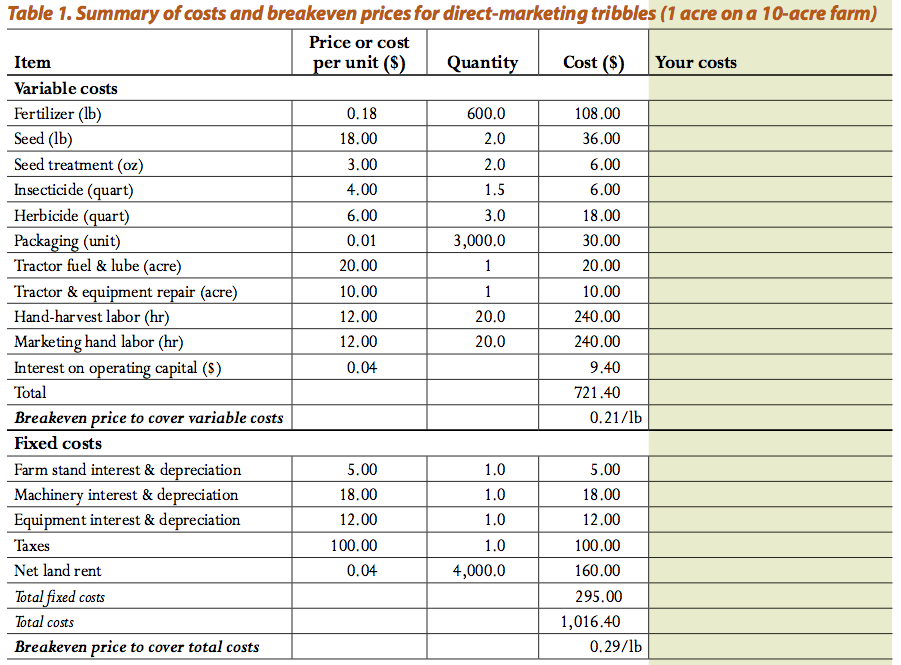

To illustrate the concepts of fixed and variable costs, a hypothetical budget has been developed for an imaginary crop called tribbles. Tribbles are an annual vegetable crop bred especially for the Pacific Northwest climate. They are a highly nutritious vegetable with an average yield of 3,500 pounds per acre. They have a long shelf life and are well-suited for farm direct marketing. Table 1 shows production costs for tribbles.

Variable costs

The typical out-of-pocket or variable costs include fertilizer, seeds, insecticide, herbicide, hired labor for production and marketing, packaging materials, repairs, and tractor fuel and lubrication. To facilitate budget revision and analysis, include both the price and the number of units (“Quantity”) in the budget. Notice that interest on operating capital is included in variable costs. Interest on investment capital is included as a fixed cost.

To calculate interest on operating capital, total all preharvest cash costs and then multiply by the fraction of the year they are outstanding. For example, if the period between planting and harvest is 4 months, then cash production costs would be tied up in the crop for one-third (four-twelfths) of the year. Multiply total variable costs by one-third and then by the cost of money (here the short interest rate is set at 4 percent per year) to find the charge for interest on operating capital. In this example it is:

$712 x 0.33 x 0.04 = $9.40

Fixed costs

Fixed costs in the budget include interest and depreciation on machinery and equipment used to produce tribbles. In this example, fixed marketing costs would include an investment in a farm stand structure. Fixed costs are in most instances more difficult to evaluate and tailor to a specific farm. This simplified tribble budget lists machinery, equipment, and farm stand ownership costs but does not describe the equipment and stand or the replacement costs for each. Also unknown is the number of acres on which the machinery is used and whether it is used only for tribble production or for other products as well. For your own summary of costs, you must analyze these factors, called assumptions (usually supplied in a narrative) to determine whether the fixed costs are appropriate and whether any added investments are required.

To simplify for this example, the tribble budget assumes that the entire farm is devoted to tribble production. In typical practice, however, several commodities are produced on the same farm with the same set of machinery and may be marketed through the same marketing facilities. Budget construction in that case requires allocating machinery and other fixed costs to each crop. Real estate taxes also are fixed costs, but since they are on a per-acre basis, it is relatively easy to assign them to a particular crop.

Land rent or land charge is assigned based on the approximate market value of the land. With a market value of $4,000/acre for land and a 4 percent interest rate, the land charge would be $160 for each acre used in tribble production. Using again the “opportunity cost” concept, we calculate the value of land by subtracting the sale cost and any capital gains tax due from estimated market value. The result is the amount that could be earning interest if the land were sold.

Tailoring a standard budget

The university Extension services in Oregon, Idaho, and Washington have developed enterprise budgets for many commodities. Budgets, however, are only as good as their assumptions. With the wide variation in possible cultural and management practices in the Pacific Northwest, it is very important to tailor published budgets to your individual farm.

The budget formats in this publication invite you to make adjustments to reflect your own production and marketing realities. Your Extension office can help with adjustments to yield and technical production recommendations. Sometimes, Extension educators have access to input and output price information. You can supplement this with additional information you receive from other growers and marketers.

The largest variable cost in the tribble production budget is 40 hours of harvesting and marketing labor, which the standard budget prices at $12 per hour. If you are not yet familiar with tribble production and marketing, you might not know whether 40 hours is a valid number, but you can evaluate the wage rate. For example, is it possible to hire farm labor at $12 per hour?

Breakeven Analysis

Notice in the last row of Table 1 that the breakeven price to cover total costs is $0.29/lb. Here is how that is calculated:

total cost ($1,016.40) ÷ yield (3,500 lb) = $0.29/lb

The difference between total revenue and total cost is net profit. Net profit in this case is the return for your risk of loss, unpaid family labor charges, and your management. If for this example the market price is $0.35 per pound, then total revenue is production of 3,500 pounds multiplied by the output price of $0.35 or $1,225. The net profit is $1,225 – $1,016.40 (total costs) or $208.60 per acre. On a per-unit-of-output basis, the difference is $0.35 – $0.29 or $0.06 per pound.

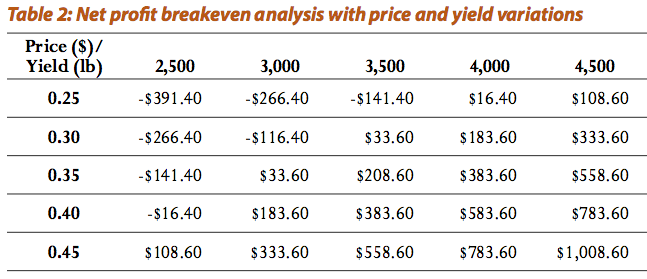

Given other uses for your land and management, is this net profit enough? Only you can judge. On the revenue side, both yield and price changes will influence your net profit per acre. Table 2 shows you how increases or decreases of both these factors will influence your net profit. The lowest price and yield combination results in a net loss of $391.40 per acre while the highest results in a net profit of $1,008.60 per acre.

Variable cost decision making

Table 1 also shows that the breakeven price to cover variable costs is $0.21 per pound. This is calculated as:

total variable costs ($721.56) ÷ yield (3,500 lb) = $0.21/lb

What should you do if, at harvest, the price for the tribble crop is $0.20 per pound? Should you plow the crop under or harvest it? To make the best decision, you need to evaluate the appropriate costs. The decision rule is that if expected returns exceed additional variable costs, then production (harvest and sale) should proceed. All fixed costs may not be covered but, as long as variable costs are more than covered, there will be some contribution toward fixed costs.

At harvest time, all production costs committed up to that point have become fixed costs. The seed and applied nitrogen and insecticides are just as fixed as taxes and machinery ownership costs. The relevant variable costs at this point are harvest at $485 (including hired labor and marketing) and packaging at $30; divided by yield:

($480 + $30) ÷ 3,500 lb = $0.15/lb

Given the $0.20 per pound crop price, you would be better off by $0.05 per pound to harvest and sell. Even though $0.20 per pound does not cover total variable costs, it does contribute something to the bundle of costs fixed at harvest. To say it another way, if you harvest and sell you will lose fewer total dollars.

Enterprise Selection

Deciding what to produce and how to sell your products are important and often quite complex decisions. This section offers a brief summary of the process of choosing one individual enterprise. Most farm-direct businesses, even quite small ones, consist of several enterprises. See the publication A Market-driven Enterprise Screening Guide (http://sfp.ucdavis.edu/files/143914.pdf) for a more complete discussion and a worksheet that leads you step by step through the most important aspects of these decisions.

The first step is to develop a list of potential enterprises. You can accomplish this by visiting different market outlets, interviewing knowledgeable people, and paying attention to what is attracting the media’s notice. Make sure you understand the requirements of each potential enterprise and whether you have the resources available, so you can determine how well it will fit your farm and help you achieve your goals. The process is similar to choosing what car to buy from among a limited number of options by developing a comparison sheet that lists the most important characteristics for you (for example, price, horsepower, trunk size, headroom, and turning radius). In the end, your choice would depend on factors such as your pocketbook and family size, driving patterns, preferences, and so on.

The enterprise selection screening worksheet compares enterprises across 38 different characteristics grouped in five categories—marketing, production, information, resources, and risk. The process requires that you gather and consider many different factors. Next, you focus on the three to five factors that you consider to be the most important. At this point, you will be prepared to either make a decision or continue to collect needed information. Enterprise selection, which is both an art and a science, will have a major influence on the profitability of your farm-direct business.

The Farm-direct Marketing Set

A farm-direct marketing business provides both attractive opportunities and unique challenges to farm families. The farm-direct marketing series of Extension publications offers information about establishing and developing a range of farm-direct enterprises.

Other publications in the series are:

• An Overview and Introduction (PNW 201)

• Merchandising and Pricing Strategies (PNW 203)

• Location and Facilities for On-farm Sales (PNW 204)

• Personnel Management (PNW 205)

• Financial Management (PNW 206)

• Legal Guide to Farm-direct Marketing (PNW 680)

• Food Safety and Product Quality (PNW 687)

To learn more, consider one of the online courses offered by Oregon State University, Washington State University, and University of Idaho:

In Oregon—Growing Farms: Successful Whole Farm Management https://pace.oregonstate.edu/catalog/growing-farms-successful-whole-far…

In Washington—Cultivating Success™ Sustainable Small Farms Education Program: http://cultivatingsuccess.wsu.edu

In Idaho—Cultivating Success™ Sustainable Small Farms Education Program: www.cultivatingsuccess.org

This information is provided for educational purposes only. If you need legal [or tax] advice, please consult a qualified legal [or tax] adviser.

Trade-name products and services are mentioned as illustrations only. This does not mean that the Oregon State University Extension Service either endorses these products and services or intends to discriminate against products and services not mentioned.

© 2018 Oregon State University.

Extension work is a cooperative program of Oregon State University, the U.S. Department of Agriculture, and Oregon counties. Oregon State University Extension Service offers educational programs, activities, and materials without discrimination on the basis of race, color, national origin, religion, sex, gender identity (including gender expression), sexual orientation, disability, age, marital status, familial/parental status, income derived from a public assistance program, political beliefs, genetic information, veteran’s status, reprisal or retaliation for prior civil rights activity. (Not all prohibited bases apply to all programs.) Oregon State University Extension Service is an AA/EOE/Veterans/Disabled.

Related publications

© 2020 Published and distributed in furtherance of the Acts of Congress of May 8 and June 30, 1914, by the Oregon State University Extension Service, Washington State University Extension, University of Idaho Extension and the U.S. Department of Agriculture cooperating. The three participating Extension services offer educational programs, activities and materials without discrimination on the basis of race, color, national origin, religion, sex, gender identity (including gender expression), sexual orientation, disability, age, marital status, familial/ parental status, income derived from a public assistance program, political beliefs, genetic information, veteran’s status, reprisal or retaliation for prior civil rights activity. (Not all prohibited bases apply to all programs.)